Board Explores the Use of Reserves to Balance the School Budget

- Category: Schools

- Published: Sunday, 10 March 2024 11:35

- Joanne Wallenstein

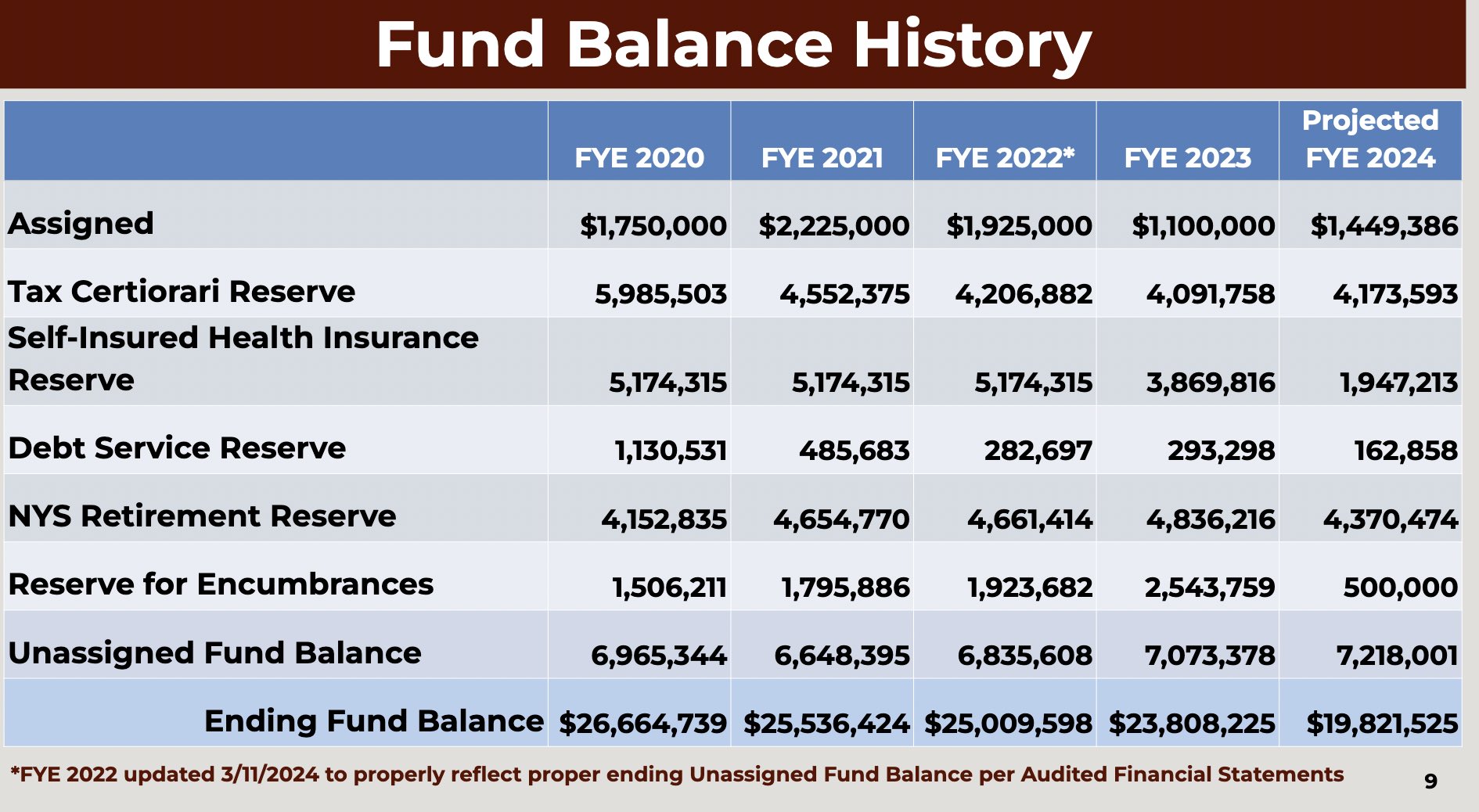

The use of the school district fund balance to keep tax increases below the tax cap while leaving the district with enough funds to meet unanticipated expenses is a subject of discussion every year. The school district maintains several types of reserves as illustrated in the slide at top. The funds are held to make payments for unexpected health insurance claims from the district’s self insured health plan or to refund taxpayers who negotiate reductions in their real estate taxes.

The use of the school district fund balance to keep tax increases below the tax cap while leaving the district with enough funds to meet unanticipated expenses is a subject of discussion every year. The school district maintains several types of reserves as illustrated in the slide at top. The funds are held to make payments for unexpected health insurance claims from the district’s self insured health plan or to refund taxpayers who negotiate reductions in their real estate taxes.

However, the portion called the Unassigned Fund Balance cannot be larger than 4% of the prior year’s budget and for the coming year the district is planning to keep that number at $7.2mm which is four percent of the 2023-24 school budget.

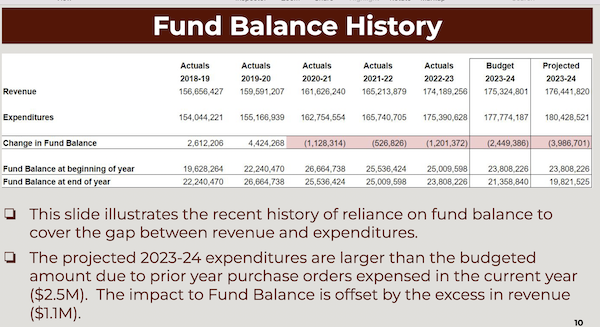

Looking at the proposed 2024-25 school budget we noted that the overall reserves are shrinking, falling from a high of $26.6mm in 2019-20 to a projected $19.8 mm at the end of the 2023-24 school year. The health reserve is projected to fall from $5.1mm in 2022 to $1.9mm for fiscal year 2024.

For the last two years, the board used fund balances to balance the budget and keep taxes below the cap: using $2.44 million in 2022-23 and $3.98 million in 2023-24. However the decrease in the fund balance means that the district cannot continue to use this strategy to fund the 2024-25 school budget.

Board members discussed the reserves at the February 5, 2024 meeting and we followed up with some questions about reserves for Andrew Lennon, Assistant Superintendent for Business.

Q: In an ideal world, how much should we be holding in reserve on a projected budget of $185mm?

A: As you noted above, the Unassigned Fund Balance is limited to 4% of the subsequent year's budget and any excess there will either need to be moved into another legal reserve or used to offset the tax levy. Each reserve has its own legally defined purpose and requires its own test of reasonableness which is verified by auditors. As Dr. Patrick and I continue to familiarize ourselves with the financial condition and long range financial picture of the district, he and I will be making a recommendation to the board regarding the upper and lower bounds for each reserve and these boundaries will guide our use going forward. However, these recommended limits will obviously be subject to the availability of funds.

Q: What has the reserve for encumbrances been used to fund?

A: The reserve for encumbrances reflects funds set aside for purchases of goods or services that have not been received at year end (6/30). Since the goods or services have not been received by the fiscal year end, the district cannot recognize the expense for these open purchase orders. Therefore, accounting standards require the district to summarize the value of those purchases and record that value in the reserve for encumbrances. Essentially, we are required to set aside funds to cover the expense in the future year so that the vendor can be paid when the goods or services are received.

At the February 5 meeting Lennon noted that the district has new accounting software which should help close out more purchase orders by the end of the school year and decrease this reserve for encumbrances.

Q: Can you explain to the community what the ramifications could be of the loss of reserves?

A: Reserves and Fund Balance provide the district with financial stability, cash flow/liquidity and demonstrate general fiscal health. The paragraph below is from the NYS Comptroller's Office Reserve Fund Guidance and I thought it helpful:

"Saving for future projects, acquisitions and other allowable purposes is an important planning consideration for local governments and school districts. Reserve funds provide a mechanism for legally saving money to finance all or part of future infrastructure, equipment and other requirements. Reserve funds can also provide a degree of financial stability by reducing reliance on indebtedness to finance capital projects and acquisitions. In uncertain economic times, reserve funds can also provide officials with a welcomed budgetary option that can help mitigate the need to cut services or to raise taxes. In good times, money not needed for current purposes can often be set aside in reserves for future use." Source:

Declining reserves has the potential to negatively impact the District’s credit rating thereby increasing borrowing costs. It can also create cash flow challenges making it more difficult to both cover payments and generate interest earnings. Finally, it could result in the inability to address unanticipated expenses without burdening the educational program.

Also, at the February 5, Board member Jim Dugan asked Lennon about the health insurance reserve for the district’s self insured health plan.

He noted that these reserves had fallen from $5.1mm in 2022 to $3.38mm in 2023 and is projected to be $1.947 mm for 2024-25.

Lennon explained that during the 2022-23 the plan had a difficult year with larger than expected claims. A million dollars was earmarked to pay those claims and was maintained in the 2023-24 budget. However, he believes that $1.97 million is an appropriate reserve for 2024-25. Dr. Patrick said the district evaluates the viability of the self-insured plan quarterly as well as annually when they sign contracts for the following year. They will continue to evaluate whether or not a self -insured plan is efficient for the district.