Board Explores the Use of Reserves to Balance the School Budget

- Details

- Written by: Joanne Wallenstein

- Hits: 3361

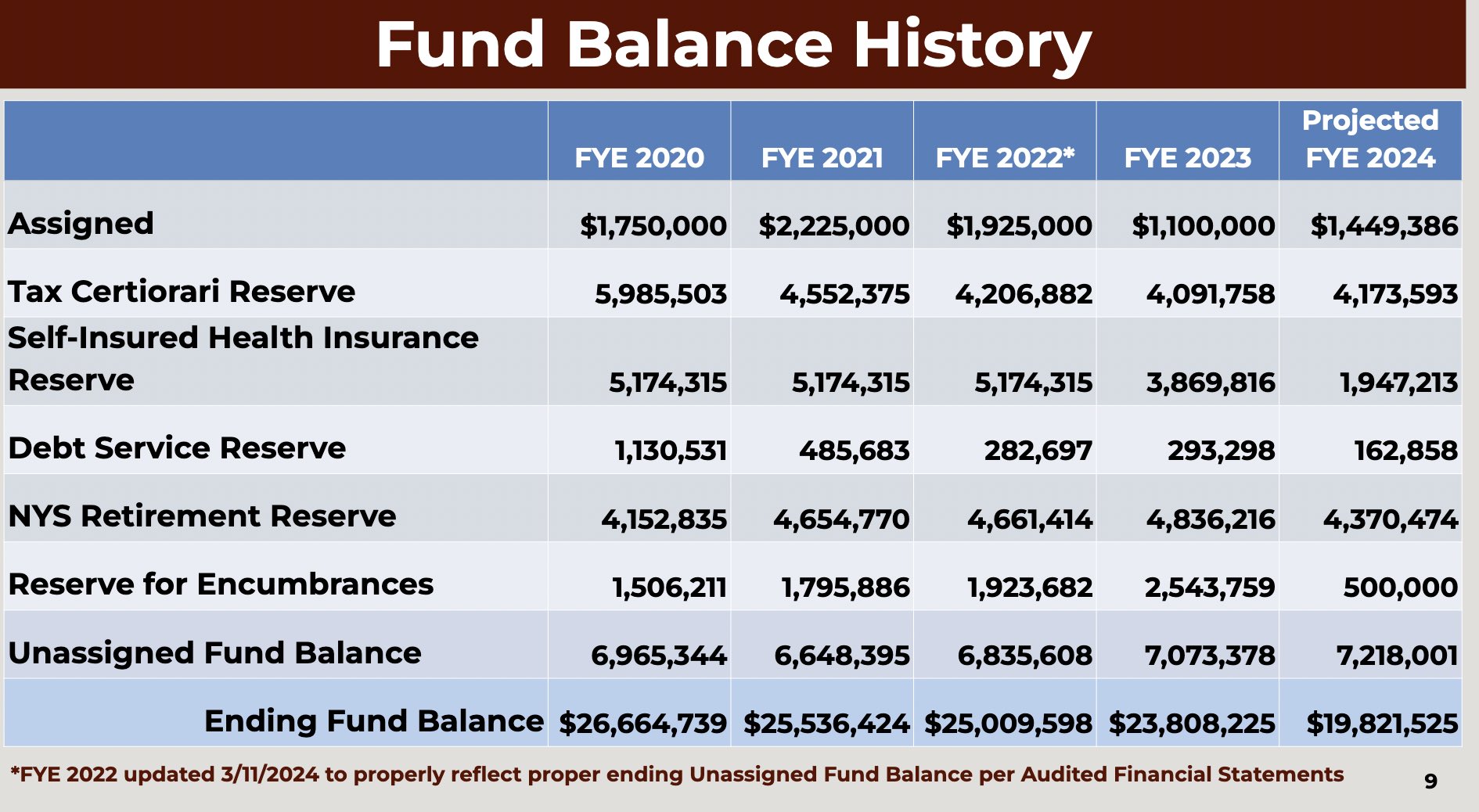

The use of the school district fund balance to keep tax increases below the tax cap while leaving the district with enough funds to meet unanticipated expenses is a subject of discussion every year. The school district maintains several types of reserves as illustrated in the slide at top. The funds are held to make payments for unexpected health insurance claims from the district’s self insured health plan or to refund taxpayers who negotiate reductions in their real estate taxes.

The use of the school district fund balance to keep tax increases below the tax cap while leaving the district with enough funds to meet unanticipated expenses is a subject of discussion every year. The school district maintains several types of reserves as illustrated in the slide at top. The funds are held to make payments for unexpected health insurance claims from the district’s self insured health plan or to refund taxpayers who negotiate reductions in their real estate taxes.

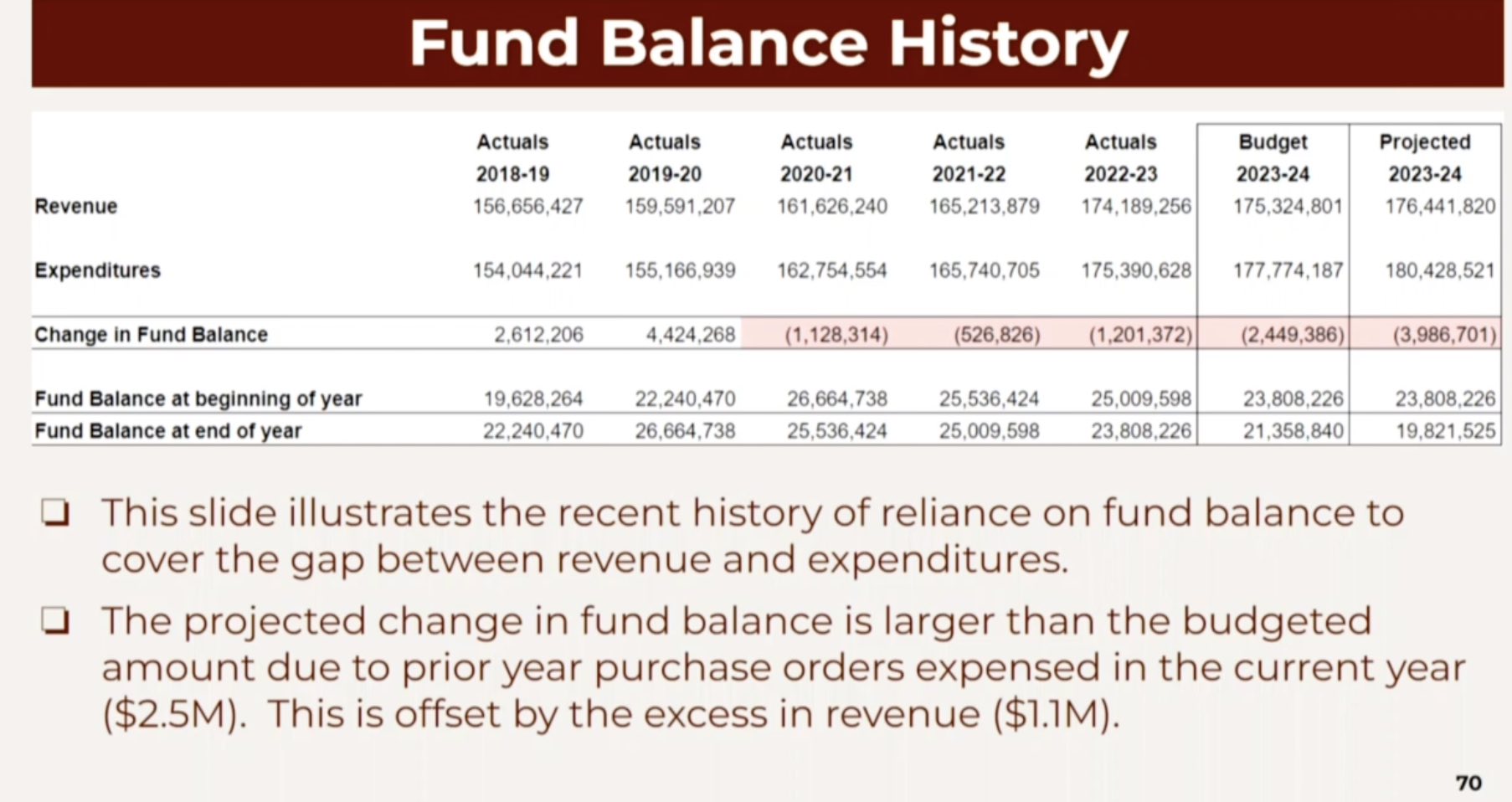

However, the portion called the Unassigned Fund Balance cannot be larger than 4% of the prior year’s budget and for the coming year the district is planning to keep that number at $7.2mm which is four percent of the 2023-24 school budget.

Looking at the proposed 2024-25 school budget we noted that the overall reserves are shrinking, falling from a high of $26.6mm in 2019-20 to a projected $19.8 mm at the end of the 2023-24 school year. The health reserve is projected to fall from $5.1mm in 2022 to $1.9mm for fiscal year 2024.

For the last two years, the board used fund balances to balance the budget and keep taxes below the cap: using $2.44 million in 2022-23 and $3.98 million in 2023-24. However the decrease in the fund balance means that the district cannot continue to use this strategy to fund the 2024-25 school budget.

Board members discussed the reserves at the February 5, 2024 meeting and we followed up with some questions about reserves for Andrew Lennon, Assistant Superintendent for Business.

Q: In an ideal world, how much should we be holding in reserve on a projected budget of $185mm?

A: As you noted above, the Unassigned Fund Balance is limited to 4% of the subsequent year's budget and any excess there will either need to be moved into another legal reserve or used to offset the tax levy. Each reserve has its own legally defined purpose and requires its own test of reasonableness which is verified by auditors. As Dr. Patrick and I continue to familiarize ourselves with the financial condition and long range financial picture of the district, he and I will be making a recommendation to the board regarding the upper and lower bounds for each reserve and these boundaries will guide our use going forward. However, these recommended limits will obviously be subject to the availability of funds.

Q: What has the reserve for encumbrances been used to fund?

A: The reserve for encumbrances reflects funds set aside for purchases of goods or services that have not been received at year end (6/30). Since the goods or services have not been received by the fiscal year end, the district cannot recognize the expense for these open purchase orders. Therefore, accounting standards require the district to summarize the value of those purchases and record that value in the reserve for encumbrances. Essentially, we are required to set aside funds to cover the expense in the future year so that the vendor can be paid when the goods or services are received.

At the February 5 meeting Lennon noted that the district has new accounting software which should help close out more purchase orders by the end of the school year and decrease this reserve for encumbrances.

Q: Can you explain to the community what the ramifications could be of the loss of reserves?

A: Reserves and Fund Balance provide the district with financial stability, cash flow/liquidity and demonstrate general fiscal health. The paragraph below is from the NYS Comptroller's Office Reserve Fund Guidance and I thought it helpful:

"Saving for future projects, acquisitions and other allowable purposes is an important planning consideration for local governments and school districts. Reserve funds provide a mechanism for legally saving money to finance all or part of future infrastructure, equipment and other requirements. Reserve funds can also provide a degree of financial stability by reducing reliance on indebtedness to finance capital projects and acquisitions. In uncertain economic times, reserve funds can also provide officials with a welcomed budgetary option that can help mitigate the need to cut services or to raise taxes. In good times, money not needed for current purposes can often be set aside in reserves for future use." Source:

Declining reserves has the potential to negatively impact the District’s credit rating thereby increasing borrowing costs. It can also create cash flow challenges making it more difficult to both cover payments and generate interest earnings. Finally, it could result in the inability to address unanticipated expenses without burdening the educational program.

Also, at the February 5, Board member Jim Dugan asked Lennon about the health insurance reserve for the district’s self insured health plan.

He noted that these reserves had fallen from $5.1mm in 2022 to $3.38mm in 2023 and is projected to be $1.947 mm for 2024-25.

Lennon explained that during the 2022-23 the plan had a difficult year with larger than expected claims. A million dollars was earmarked to pay those claims and was maintained in the 2023-24 budget. However, he believes that $1.97 million is an appropriate reserve for 2024-25. Dr. Patrick said the district evaluates the viability of the self-insured plan quarterly as well as annually when they sign contracts for the following year. They will continue to evaluate whether or not a self -insured plan is efficient for the district.

School Board Weighs Community Tolerance for a Budget that Exceeds the State Tax Cap

- Details

- Written by: Wendy MacMillan

- Hits: 4254

The Board of Education held a marathon budget study session on Monday, March 4th where members of the board spent hours, thoughtfully discussing all of the varying factors that shape the proposed 2024-2025 school budget. At the meeting, BOE members learned about proposed budget funds for curriculum, instruction, and assessment, special education and student services, safety, security, and emergency management, interscholastic athletics and technology and innovation. You can watch the presentation on the school website.

The Board of Education held a marathon budget study session on Monday, March 4th where members of the board spent hours, thoughtfully discussing all of the varying factors that shape the proposed 2024-2025 school budget. At the meeting, BOE members learned about proposed budget funds for curriculum, instruction, and assessment, special education and student services, safety, security, and emergency management, interscholastic athletics and technology and innovation. You can watch the presentation on the school website.

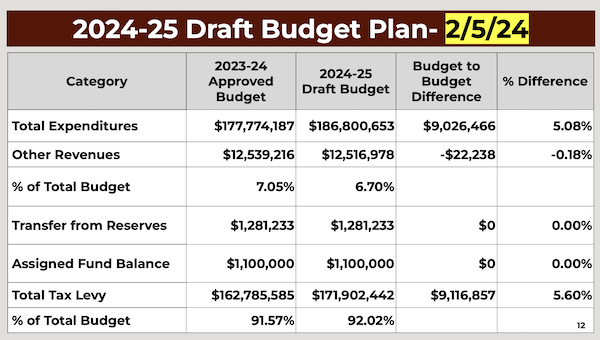

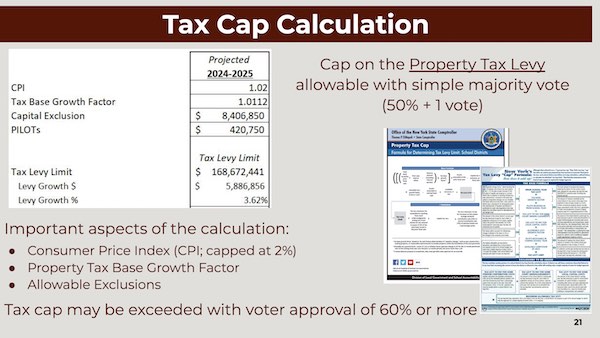

At the previous budget study session on February 5, the administration proposed a 2024-25 school budget of $186.8 mm which would require a 5.6% tax levy increase over 2023-24, exceeding the allowable tax cap of 3.63%. At the March 4th session, they scaled back some of their requests , and reduced the increase in the levy to 4.95%, which is still in excess of the state tax cap. This translates to a 5.26% increase for Scarsdale taxpayers and a decrease of 8.09% for those in the Mamaroneck Strip.

If the Board does propose a budget that exceeds the tax cap, it requires a 60% approval from the community, rather than a simple majority vote.

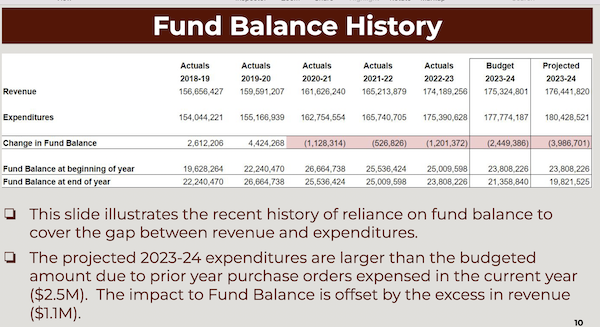

Since 2020, the Board of Education has used the fund balance to keep tax increases below the cap, but reserves are diminishing administrators say this is no longer a good way to balance the budget.

In the following statement Superintendent Dr. Drew Patrick explained where we now stand:

Referring to the slide above he said, "Here is a summary of the budget we presented on February 5, 2024. As a reminder, that budget included 8.9 new full time equivalent positions, some of which are currently in place because they were added through the utilization of budgeted contingency positions. This plan included total expenditures of $186,800,653, representing a $9,026,466 or 5.08% increase over the current year budget, and a projected tax levy increase of 5.60%, nearly 2% or $3.2 million above the tax cap of 3.61%. I want to acknowledge that this came as something of a shock to members of the Board, and certainly to the community, but it reflects the reality that we can no longer do everything we want to do within the confines of the tax levy limit. Indeed, even with the reductions from the preliminary budget that we are proposing tonight, the budget plan currently remains over the tax cap. This is a budget I, and my team, strongly support because we believe it reflects the program we need, and the community expects. With your indulgence, I would like to spend a little bit of time putting this year in the context of the recent past before moving on to the cuts we are proposing and the revised budget draft.

Referring to the slide above he said, "Here is a summary of the budget we presented on February 5, 2024. As a reminder, that budget included 8.9 new full time equivalent positions, some of which are currently in place because they were added through the utilization of budgeted contingency positions. This plan included total expenditures of $186,800,653, representing a $9,026,466 or 5.08% increase over the current year budget, and a projected tax levy increase of 5.60%, nearly 2% or $3.2 million above the tax cap of 3.61%. I want to acknowledge that this came as something of a shock to members of the Board, and certainly to the community, but it reflects the reality that we can no longer do everything we want to do within the confines of the tax levy limit. Indeed, even with the reductions from the preliminary budget that we are proposing tonight, the budget plan currently remains over the tax cap. This is a budget I, and my team, strongly support because we believe it reflects the program we need, and the community expects. With your indulgence, I would like to spend a little bit of time putting this year in the context of the recent past before moving on to the cuts we are proposing and the revised budget draft.

How does this budget compare within the context of recent budgets and tax levies?

We understand the impacts of the tax cap as a check on a period of historically large tax increases (1990’s and 2000’s), but also as a constraint to school board flexibility. Nonetheless, over the past 10 years, our average budget to budget increase is 2.14%, and our average tax levy increase is 2.23%. Over that same time period, our tax levy was below the tax cap by an average of $453,117, or a cumulative $4,531,166. Thus, it is understandable that our preliminary proposed budget may seem inconsistent with this recent past. Notably, one of the ways we have stayed under the cap in recent years has been through the reliance on the use of fund balance to offset expenditures in excess of revenue. That, of course, is not a sustainable practice over the long run, and we are starting to see the impacts of that practice. Andrew will discuss this in more detail later this evening.

Why did we start with such a large proposal?

There are three main reasons for this. First, we are sharing our authentic internal process more transparently than in the past. Second, we have significantly expanded our programs and supports for students in recent years. This has been in response to community expectations, and has been accomplished without exceeding the cap (though see note above about fund balance). Third, inflation and unavoidable cost increases in certain areas have reached a tipping point. Below, I have included detail to each of these reasons.

Our Process

Being quite new to the role of Superintendent, I took the opportunity last year to view the Board-Administration budget development process with fresh eyes. While I played a role in this process in each of my years in Scarsdale, since becoming Superintendent, I have grown to believe that the Board should have a more comprehensive understanding of and transparent window into the internal deliberations that shape the Superintendent’s proposed budget. Thus, starting with last year’s budget, we presented a budget that authentically included our desired program, operational, and capital elements to fulfill our educational goals and objectives, irrespective of the tax levy. This marked a starting point for discussion, deliberation, inquiry, and dialog, both at the Board table and in the community. Over the course of the public budget development process, the Board made informed judgements about the balance between cost and affordability. For those who observed or participated in the process last year, the result--a budget that came in under the tax cap--was only achieved after weighing alternatives, eliminating line items that were initially requested, and making strategic choices about what budget items would have a greater or lesser impact toward our desired student outcomes. Essentially, we aim to replicate that process this year, though the other two reasons stated above will make this process much more difficult this year.

Program Expansion

In any given year, the major budget to budget drivers tend to be contractual salary increases, mandated pension system increases, and benefit increases, particularly in the area of health insurance. Of course, staffing and program additions increase the base budget as well. I think it helps to frame increases both generally and with respect to the preliminary 2024-25 budget, around two frequently asked questions.

Understanding that salaries and benefits (i.e., people) account for 80% of the overall budget, why is the budget going up more than 2% when our labor contracts have kept salary schedule increases to below 2% (recently between 1.5-1.75%)?

Why do we need more staff when enrollment is stable?

It turns out that these questions are interrelated. It is true that our contractual salary increases have been modest, and well below the recent high inflation. In the past ten years, the major driver of our budget increases have been the result of added positions. Over that time, we have added roughly 49 new teacher positions, all while staying under the tax cap. Each of these positions was carefully vetted, and resulted in the introduction of new programming or expansion of existing programming. For example, we introduced a robust STEAM sequence and expanded electives at the high school, significantly increased our mental health staffing to support students and families, and have greatly enhanced our continuum of services and related services supports for special education students. These FTE additions were proposed because they align with our guiding principles of staffing, and they reflect the resources necessary to meet the needs of our students and expectations of our community.

On top of the above, we have also added a safety, security, and emergency management structure inclusive of a Chief of SSEM, and safety monitors at all buildings. This has created a recurring (and escalating) annual cost in excess of $1 million.

Inflation and Cost Increases

The pressure of inflation on goods and services, coupled with cost increases in health insurance, mandated retirement contributions, has largely been absorbed over the years by pushing our budget to the limit, and foregoing some of the desires and requests that come in. While in the past we have been able to generate fund balance by having actual costs that come in below budgeted expenditures, since the end of the 2019-20 school year, this is no longer happening. One representation of this can be found in the $4,531,166 in allowable tax levy under the tax cap that we have elected not to levy and expend. Put simply, we have tightened our belts in response to cost pressures so we could build out the programs described earlier. We are no longer in a position to do this without making difficult choices. Thus, we simply can’t do everything we want to do and that we think is important for our students and families without exceeding the tax. If we think the support of this is not attainable, then we will need to examine ways to reduce our expenditures and make choices about what to keep and what we want to cut. The next several slides will explain the changes we have made to the preliminary draft budget plan.

First, in the past month we have re-examined the entire proposed budget, and not surprisingly we have found a few areas where either our assumptions or our data entry have required revision. There are two items that were not accounted for at the level we expect, and thus they have resulted in adjusted expenditures of an additional $180k.

Our proposed expenditure reductions begin with salary, wages, and benefit costs. We are proposing to defer two of the three special education teaching positions we presented in our staffing recommendations- 1 at SMS and 1 at SHS. At the middle school, the 1.0 position that remains in the proposed budget accomplishes the expansion of the Integrated Co teaching program from 6th grade into 7th grade. The elimination of the second position at SMS, and the elimination of the position at SHS, leaves us at or close to our mandated ratios in the LRC program with decreased scheduling flexibility and little room for new student classifications. Eric will speak more to this during the Special Education budget section.

Next, we reduced the overall elementary staffing assumption by 2.0 FTE, which reflects the elimination of 1 of 2 contingency positions that were proposed, as well as returning a teacher on special assignment to the classroom next year. The final reduction in this area reflects a more precise measure of expected pension costs for civil service employees. This amounts to $705k in reductions.

We have identified another $263k in reductions from equipment, supplies, and BOCES codes. A budget duplication was identified, we scaled back the bus radio purchase by about 25%, we slow down but do not eliminate our deployment of new cameras and door ajar sensors, and defer a needed replacement time-clock system for hourly employees.

Finally, we have made four revisions to contractual codes that would reduce reliance of charter buses for athletics, replacing some trips with school buses, revises our liability insurance premium, removes more duplicate expenses, and suspends (perhaps temporarily) our association with the Advancing Literacy initiative, totalling $285k in reductions. Together, these cuts result in $1,061,281 less expenditures.”

What’s Next

It’s clear that administrators are still greatly wrestling with how to deliver the kind of stellar educational programming that Scarsdale residents have come to expect, while staying within the confines of a state mandated tax cap.

Board President Ron Schulhof said, “This year’s budget is especially challenging, in part due to numerous impacts out of our control. For example, the Governor is proposing a significant cut to our State Aid which we are very actively working to get restored. We have also experienced large increases in health care costs and other operating costs, which are impacting school districts throughout the State.

With so much at stake for the community, Schulhof encouraged all Scarsdale residents to participate in the Budget Study Meetings so that they have a more firm understanding of the nuances and factors that contribute to the budgeting process before deciding how they will vote in May.

Before the next Budget Study Session Dr. Patrick asked the Board to consider questions such as: Where does the Board stand on the proposed budget? What is our tolerance for exceeding the cap? What choices are possible? And should we make more cuts to get below the cap?

Patrick explained that more cuts might mean eliminating additional staff including a half time math teacher at the high school, a special education administrator and some clerical help.

Cost savings in curriculum and extracurricular programs might include reducing arts/aesthetics consultants, cutting back program improvements and reducing the purchase of books for elementary school classrooms.

For athletics, Varsity B teams, their coaches and transportation costs could be cut.

Further savings could come from cutting the budgets for instructional and non-instructional materials and supplies, classroom furniture, the expansion of wi-fi to the hallways and non instruction IT purchases.

All this will be discussed at the next budget study session on March 11, 2024.The Board will formally adopt a budget on April 8 and the Budget Vote and School Board election will take place on May 21, 2024.

Non Sibi? Scarsdale Senior Price Gouges Fellow Students for Post-Prom Party Tickets

- Details

- Written by: Joanne Wallenstein

- Hits: 9768

This letter to the editor was written by the parent of a Scarsdale High School senior:

This letter to the editor was written by the parent of a Scarsdale High School senior:

It was shocking and disheartening to learn that the Scarsdale High School senior who is selling tickets to the prom after-party in NYC is price gouging his fellow students for his personal benefit.

Each year there is a senior who takes it upon themselves to sell tickets to the prom after-party at a club in NYC. Normally the student makes a small profit as compensation for their coordination effort. This year however the student is poised to make tens of thousands of dollars as he has created a special scheme to price gouge his fellow students for his own behalf.

The way it seems to be working is that he released a very small (~50) number of tickets available for sale at a set time for $100/each. Those tickets sold out quickly and most students were not able to get them. Then he released a similarly small batch of tickets for sale at $115/ticket which also sold out quickly. The next batch is supposedly soon going on sale for $130/ticket (!!).

As there are 400 kids in the senior class, and some people take dates to the prom, this student is making a hefty sum from his sales. It seems likely that the student was already making a profit at the $100/ticket price, and that the markups above $100 are pure profit for him.

Who are the parents of this student? Where are they and how are they allowing this?

Also, is this income is being reported to the IRS? Assuming that this student is going to college somewhere in the fall, he should be worried about continuing his scheme as there are now many angry students and parents.

Non sibi? Where has this student been for the last 4 years.

Scarsdale Parent Refutes Claim that Racial Slurs Came from the Stands at Basketball Game

- Details

- Written by: Joanne Wallenstein

- Hits: 8423

A Scarsdale parent is refuting claims of racial slurs that purportedly shut down a Varsity B girls basketball game on February 10 at Scarsdale High School. Jason Paris, a dad who was in the stands for a Girls Varsity B Basketball game against a team from East Ramapo said that no racially charged words were uttered. Contrary to what he heard while at the game, NBC news, the Journal News and News 12 reported that racial slurs had come from the stands.

A Scarsdale parent is refuting claims of racial slurs that purportedly shut down a Varsity B girls basketball game on February 10 at Scarsdale High School. Jason Paris, a dad who was in the stands for a Girls Varsity B Basketball game against a team from East Ramapo said that no racially charged words were uttered. Contrary to what he heard while at the game, NBC news, the Journal News and News 12 reported that racial slurs had come from the stands.

According to Paris, whose daughter is a junior and plays on the team, it was a referee’s call, not a racial slur that caused the game to end halfway through the fourth quarter.

Paris says, “Nothing remotely close to what is being reported happened at the game. It was the last game of the season for both teams. It was a normal game up to halfway through the fourth quarter when one of the Ramapo girls committed a foul. When the same girl had a second foul called against her the East Ramapo coach began berating the referees about foul calls. He said, “that’s it, we’re done” and the referees declared the game over and left the court. At the time, the score was 34-22 in favor of Scarsdale.

Paris says “There were only 12-14 fans there including grandparents, parents and younger siblings of the players.” He continued, “We were all sitting together and nothing negative of any nature was said. We were cheering good plays of both teams.”

Since the game was a fundraiser for breast cancer, students came in an out of the gym to sell t-shirts and at one point the Varsity A girls were in the gym to hang their senior game banners.

Paris continued, “It ended when the game was forfeited. The East Ramapo coach yelled at the refs who called the game and walked out. The Scarsdale coach gathered her girls on the bench and they left the gym to go to the locker rooms to change and say their season goodbyes.”

Paris explained that the Scarsdale players were unaware of any of these allegations and only learned about them when they received a text from one of the girls on the Scarsdale Varsity A team who was in the gym. She reported that a girl from East Ramapo said someone called her the “N” word. Paris said that girl was on crutches and did not play in the game.

Paris is a longtime Scarsdale resident who has been watching his kids play for the past 15 years. Commenting on the incident, Paris said, “As someone who was there, it’s incredibly frustrating because you can’t prove a negative. There is nothing that can be done to dispel this. The game was livestreamed with audio. The camera and audio were on and all you hear is cheering for all teams* …. Seeing this on the news, from parents who teach their children to never do anything hateful is devastating. Parents and girls are very upset at what appears to be a total fabrication.”

(*It appears that the game video has been taken down.)

Proposed 2024-25 School Budget Increase to Exceed the Tax Cap, Plus 2024-25 School Calendar Adopted

- Details

- Written by: Wendy MacMillan

- Hits: 4577

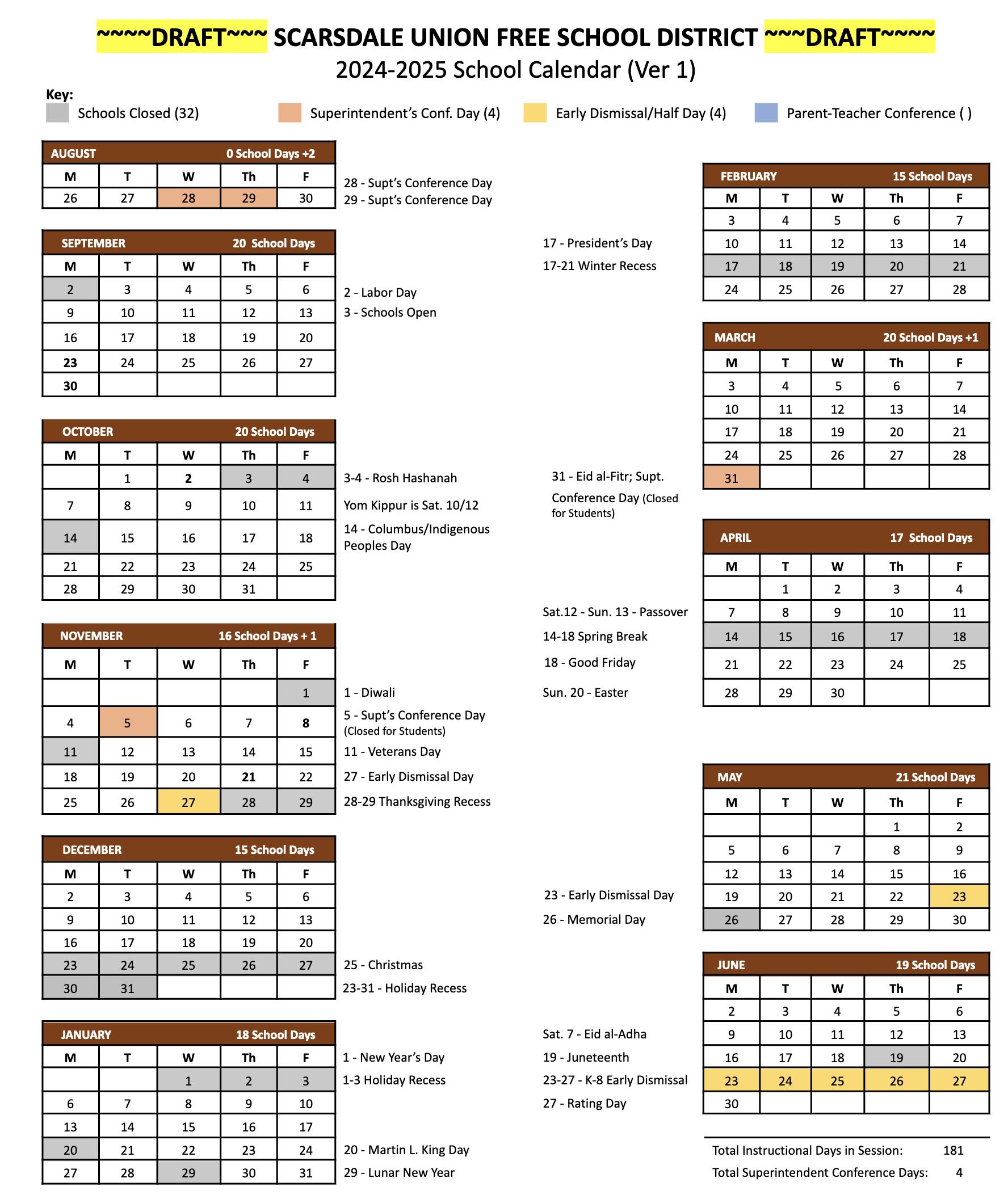

Big news from the school board this week: There will be another two week break for the holidays for the 2024-25 school year. The board adopted this calendar option at their February 5 meeting, following their second budget session for the 2024-25 school year.

Big news from the school board this week: There will be another two week break for the holidays for the 2024-25 school year. The board adopted this calendar option at their February 5 meeting, following their second budget session for the 2024-25 school year.

On the budget front, the administration increased their request for staffing for 2024-25 to include an additional dean at Scarsdale High School to decrease the existing dean’s caseload and to allow more students to go into the Civ Ed program. The total proposed staff increase now stands at 9.9 FTE’s (full time employees.)

The increase in salaries, retirement contributions and health benefits along with other expenses adds up to a proposed $9.1 mm budget to budget increase, translating to a 5.6% increase in the tax levy at a time when the state tax cap is projected to be 3.62%. If the final budget increase does exceed the cap, a 60% passage rate would be required.

The fund balance from June 30, 2023 to June 30, 2024 is expected to drop about $4mm from $23.8 million to $19.8 million.

Introducing the budget discussions, Superintendent Dr. Drew Patrick emphasized that “The school budget provides the necessary financial resources to operate the school district and to help achieve the goals and objectives of the School District.” He went on to outline our District’s goals as they are defined in our Mission and Purpose statement:

“The Scarsdale Public Schools seek to sponsor each student’s full development, enabling our youth to be effective and independent contributors in a democratic society and an interdependent world.”

Dr. Patrick also made clear that the Budget is structured to support three spheres of our School District’s organization:

-Teaching and learning which includes items such as, appropriate class sizes, rich and enriching offerings, and professional development.

-District Operations including student and staff safety, sound fiscal stewardship, strategic capital planning and attention to infrastructure, and talent recruitment/retention.

-Student Support which encircles special education, MTSS Counseling, wellbeing, and community partnerships.

Dr. Patrick concluded by stating that “Items only appear in the draft budget after much careful consideration.”

Dr. Partick first explained the additional staffing recommendation. At the January 22nd meeting, BOE members were presented with an overview of staffing recommendations for the 2024-2025 school year. In that presentation, members were informed that Tier 1 recommendations included Overall: 4.7 (new) + 2.0 Elementary + 2.2 Secondary = +8.9 FTE. The presentation went on to describe Tier II recommendations (requests that are not being proposed at this time, but are worthy of further consideration in future budget planning) which included a request from Scarsdale High School for a new Freshman Team (3.0 FTE).

He said, “We are requesting the addition of a Freshmen Civ Ed team, which requires an additional 3.0 FTE as follows: one dean* (counselor), one English teacher, and one Social Studies teacher. There are currently 356 8th graders at the middle school; the additional counselor would reduce freshman teams to 42 to 45 (currently approximately 50) students per counselor. Adding a dean would also reduce the average caseload of all deans (from ~190 to ~170 students per dean). For the 2023-24 school year, there were 190 requests for Civ Ed, and the 4th section would have allowed us to meet all of them. We believe this request is in line with the strategic plan by creating student-centered opportunities and environments by meeting student choice.”

At this prior meeting, there were a lot of questions from Board Members about why this request wasn’t considered as a Tier I recommendation. Many of the members expressed their belief that an extra team at SHS would have great benefit for teachers, students, and deans alike. Since having an extra dean (SHS Deans are guidance counselors who work with students from grades 9-12, including supporting students through the college application process), seemed especially beneficial, some members also expressed their interest in having a phased in approach to hiring a complete Freshman Team starting with hiring just a dean for the 2024-2025 school year.

Administrators promised to look further into this strategy as an option and at the BOE meeting on February 5th, SHS Principal Ken Bonamo was present to discuss the benefits of hiring an additional dean for next year and how the phased-in approach would work. Bonamo emphasized that one of the greatest impacts would be seen in the decrease of caseloads for each of the deans allowing them to spend a more optimal amount of time with each of their students.

Having taken all of this information into consideration, the new staffing recommendation was updated to include the hiring of one dean at SHS bringing the new request to a total of 9.9 FTE.

Assistant Superintendent for Business, Andrew Lennon gave an overview of the 2024-25 draft budget plan including the consideration of key components such as expenditures, revenues, fund balance, and the tax levy limit. Here are some of the highlights:

The proposed 5.60% tax levy limit exceeds the projected tax levy limit of 3.61%.

The proposed 5.60% tax levy limit exceeds the projected tax levy limit of 3.61%.

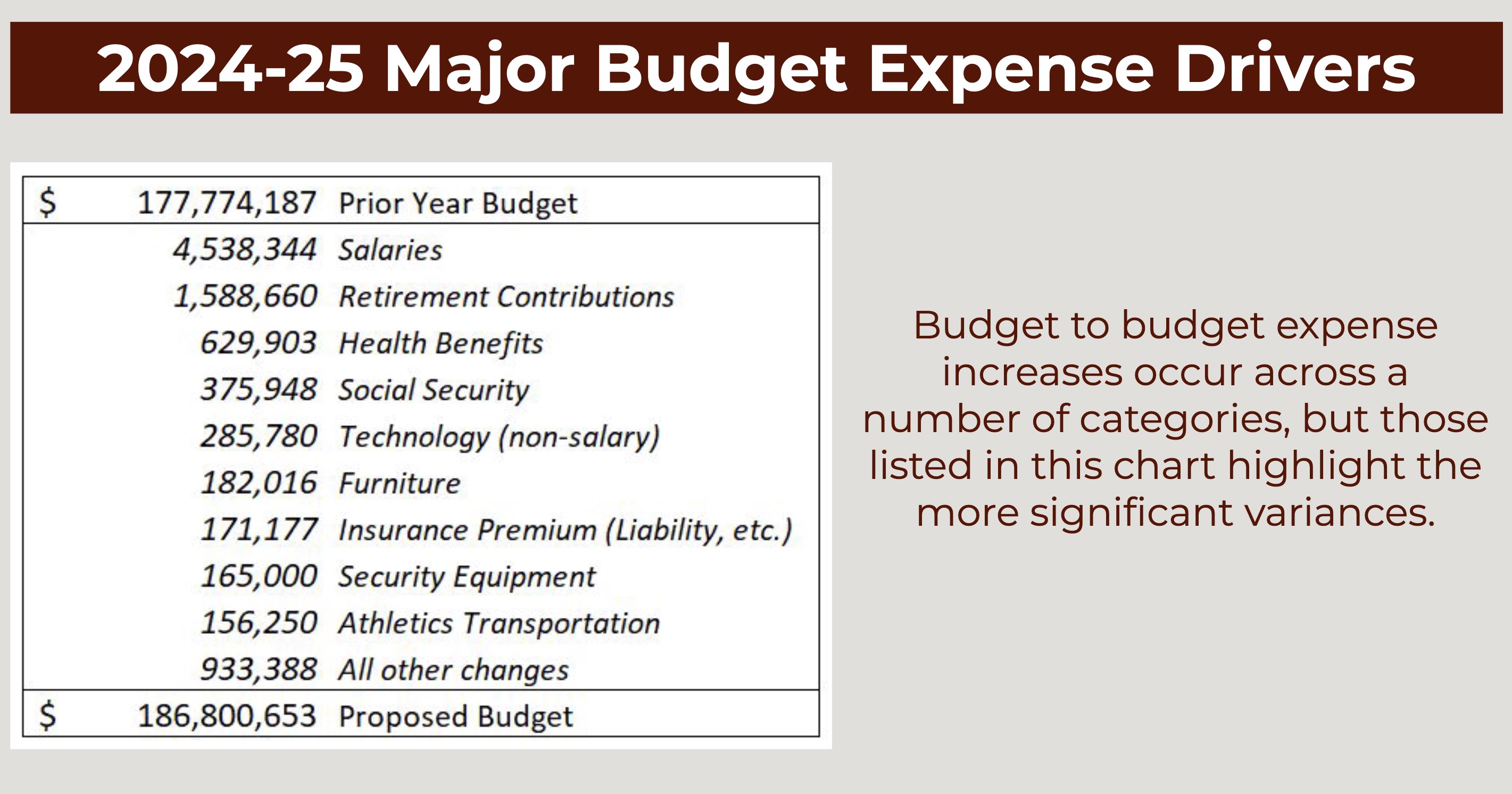

Above are the major budget expense drivers.

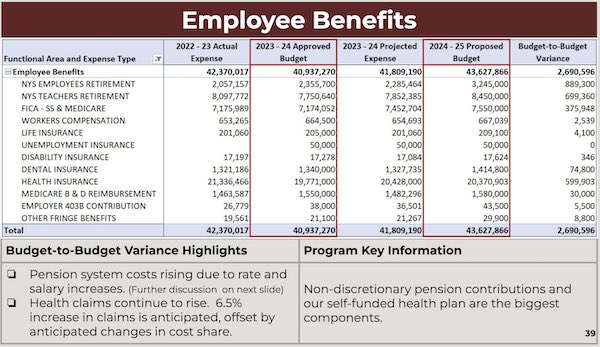

Lennon focused on these four components: Transportation, Facilities and Operations, Debt Services and Employee Benefits.

Transportation

Increases in the budget for transportation are due to the cost of maintaining an aging fleet of buses. Some older parts are not even sold anymore. Lennon explained that the department spends a lot of time and money ensuring that old buses pass inspections and struggles to keep them on the road. He discussed the needto purchase a new communication system as the existing radio system is antiquated and beyond repair and is a pressing concern for the safety of students and drivers.

Employee Benefits

The increase in expenses is largely due to rising pension systems costs and an increase in health claims.

In comments from the Board, Ron Schulhof remarked that the 5.6% increase to the tax levy is a lot, and wondered if the BOE would be open to having a discussion about possible areas of the budget that can be postponed or delayed, i.e. what budget items are “must haves” vs. “nice to haves” to see if the draft budget could be culled down. All board members members were open to having that discussion as they have done in years past.

During the public comments, Mayra Kirkendall-Rodriguez asked for more context for the budget and said it is hard to forecast financial needs without a strategic vision and a long-term financial plan which she urged our District to create.

Rachana Singh said that the draft budget is very high in a year that the Village plans to go over the proposed tax levy as well. Singh urged the BOE to adopt a fiscally responsible budget. Singh also stated that she is very supportive of the Special Education program in our District but would still like to see the data that supports the District's claim that the students in the program are thriving. She wondered if there are any metrics in place that can evaluate the data to show that students are indeed making gains. Lastly, Singh stated that she agrees with Kirkendall-Rodriguez and urged the District to create a long-term financial plan.

School Calendar

The Board adopted a school calendar for 2024-25 that starts on Tuesday September 3 and includes a two-week break during the holidays. The Board recognized that this might be a hardship for some working families, but said that moving forward the calendar would be re-evaluated based on where the holidays fall and other factors. You can see the 2024-25 calendar here:

Retirements:

Meghan Troy announced the following retirements:

From Fox Meadow Elementary School: Psychologist Jennifer Batterman and teachers Beth Kaplan, Barbara Laman, and Peter McKenna.

From Heathcote Elementary School: Teacher Katherine Bescherer.

From Edgewood Elementary School: Teacher Connie Leviatin.

From Scarsdale Middle School: Teachers Andrew Verboys, Lisa Bryan, Adam Nichols, and Yurry Buckler.

And from Scarsdale High School: Teachers Sheilah Chason and Joseph DeCrescenzo.